“20% off” is something most of us only encounter in the form of a sale sign or a coupon, am I right? We don’t think of it in terms of our income for a variety of reasons. One of these is that there’s usually a disconnect between what we earn and what we spend, because we don’t usually think of “things we are doing” as “spending.” Another reason we don’t think of our cash flow in percentages is that most people just don’t think that way. I know, because I’m not a numbers person. I’m not a numbers person in the same way that I’m not a maps person. That’s okay, because what we’re going to do right now is to tell stories and talk about broad concepts. I promise, few numbers involved.

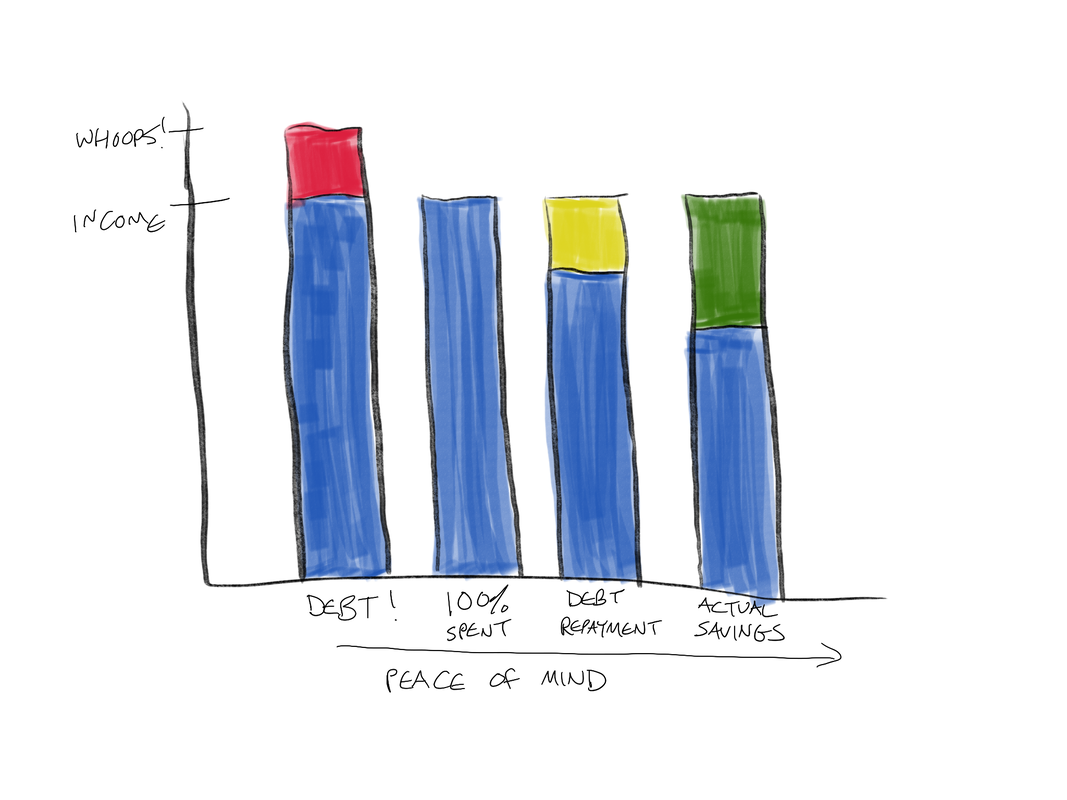

This is basically how it works. Money flows into and out of our lives. We worry about it more when we have more bills than we do money, and less when we feel like we can relax a little. Few of us were really taught about personal finance, and even if we were, our friends, family, neighbors, and colleagues are unlikely to compare notes with us. The only way we can really tell how we’re doing is by instinct and guesswork. Even married couples may not share finances, only discussing it at tax time and only when we can’t avoid it. How many of these things are true for you? Thinking of how much you earn in terms of your hourly rate Thinking of how much you earn in terms of your annual (gross) salary Thinking of how much you earn in terms of your take-home pay, paycheck by paycheck Not having thought about it for a while Honestly, none of this ever occurred to me when I first started drawing a paycheck. I thought of what I earned by the hour, and I had no sense of how much I actually took home in a month or a year. I knew how much my rent was, but it also never occurred to me to estimate how much I spent in a month on everything all together. I just did the best I could, one paycheck at a time. Life was hard, sometimes harder, sometimes even harder than that. Work hard, I thought, just keep working hard and things will get better. Things did get better eventually, but not because I worked harder. In fact I doubt I’ve ever worked as hard as I did in the days when I was flat broke. What changed was just that I understood more. I thought I would eventually get promoted if I just worked hard enough. Instead, it turned out it was completely up to me to choose a very specific career path, sign up for loans and earn an advanced education, and market and promote myself. None of the employers for whom I worked in the first decade of my career ever would have had a place for me. If I’d stayed, it never would have mattered how hard I worked, it would have gotten me nowhere. I was proud of myself for not having a credit card. I didn’t realize how complicated it would be to have no credit history later on. I took on bottom-dollar side hustles, not understanding that I would have been better off using that time to figure out how to earn more money for less effort. What I was doing was offering lower-value services, which effectually cheats people of my best contribution. Do what only you can do, not what almost anyone can do. Okay, so the first reason you aren’t saving 20% of your income is that you probably don’t know exactly how much you earn or how much you spend. Cash flow is a metaphor in your life, not a highly specific quantity. The second reason you aren’t saving 20% of your income is that you’re barely making it. You feel stuck and you don’t know what to do next to maximize your income. The third reason you aren’t saving 20% of your income is that, if you have a partner (spouse, romantic partner, roommate, kid), you aren’t discussing money. Not if you can avoid it! Bringing up the topic is a source of stress, not power. You’ve probably already fought about it, and in fact maybe you fight about it every single day. Nothing productive is going to come out of this state of affairs. Let me put it out there that for most people, what’s needed is a paradigm shift, or a completely different way of looking at the problem. (Money isn’t a problem! Instead it’s a solution for nearly every problem that modern people face). (For most of human history, your problems would have been stuff like siege warfare, plague, top-tier predator attacks, famine, and the million bajillion things that hadn’t been invented yet). It’s like this. If you make a certain amount of money and you spend all of it, you’re saving zero. If you make a certain amount of money and you also put a certain amount on credit cards, you’re spending more than you earn. You have your reasons, yes, and unfortunately banks and creditors don’t care about those. Future You is the one who’s going to have to deal with it, and Future You is NOT going to thank Today You for passing it on. If you spend 20% more than you earn, you can’t just save 20%. That only gets you back to saving zero. (This is the numbers part, but hang on, it’ll be over quickly). You have to do 40%. Right? And a little more than that to take care of the interest charges, fines, fees, and every other way the banks like to pull things out of your wallet. This is why you aren’t saving 20%. Because if you’re like most Americans, you can’t even save zero. You’re going under a little bit more each month, and the process is so gradual that you don’t even feel it happen. It doesn’t have to be like this! This isn’t a cause for being scared or angry or hopeless or defeatist. It should be more like the day I accidentally pumped liquid hand soap onto my toothbrush and noticed right before I put it in my mouth. Wait! Toothpaste isn’t pink! As long as we’re paying attention and we’re aware of what we’re doing, there’s always time to make a change. We can figure it out. Step one: Make it as fun and relaxing as possible to hang out at home, with your friends, at the park, at the public library, at the beach, or anywhere else that doesn’t cost money. Nap, read, have long conversations, draw, stretch, listen to music, make art, learn to cook, and remind yourself that contentment is free. Step two: Tell someone. Our culture is super-freaky-weird in that we’ll be totally open and honest about, say, ingrown hairs, or embarrassing first dates, or our sexuality, but not about money. Wouldn’t money seem to be the least intimate and least personal of these things? It’s just numbers, after all. But no. It IS weird. That’s why it’s an act of real bravery and courage to tell the truth about your financial anxieties and confusions. Guaranteed, you’ll find someone else who feels the exact same way you do. Maybe you can work together to learn more, or at least work together to hang out and not spend money together a lot. Step three: Think of some ways you could radically restructure the way you live, at least temporarily. As an example, my husband and I sold our car and moved into a studio apartment, at least for a year. We’re saving 40% of our income, and working on increasing that number. It isn’t all that bad because we’re usually working anyway, because it helps us feel like a team, because we got rid of most of our stuff, because it makes a good story, because the apartment has a pool and a hot tub, and because eventually we know we can move into a bigger place again. If we want to. More money, in our society at least, means more options. More choices, more freedom. If you’re curious and the spirit moves you, maybe you could get a sheet of paper or set up a spreadsheet. Maybe you could work out your net income and your average monthly expenses. Maybe you could make a list of how much you owe on all your cards, car loan, student loan, personal loans, or anything else. Maybe you could look at that number and just... feel it for a minute. Feel that you are part of a world of infinite choices and possibilities, and that a year from now, everything about that number could look and feel completely different. It’s just a number, after all. Comments are closed.

|

AuthorI've been working with chronic disorganization, squalor, and hoarding for over 20 years. I'm also a marathon runner who was diagnosed with fibromyalgia and thyroid disease 17 years ago. Archives

January 2022

Categories

All

|

RSS Feed

RSS Feed