|

It appears that much of the world is ready to move on from the great pandemic of 2020, even though more people have died of COVID already this year than in all of last year. That’s a big lesson to take away from all this, that commerce largely continued in spite of everything.

This is why it’s a particularly good time to think about how many vehicles you have, why you have them, how they affect your life, and how much they cost. How many people out there still have a two-vehicle household, even if both those cars mostly sat idle all of last year? How many people are still paying to insure two vehicles (or more), even when one or more members of the household may be working from home for the rest of their career? How many people are still paying on dormant vehicles even after they’ve started having a lot more things delivered? My husband and I got rid of our car over four years ago, and it’s been a big lifestyle upgrade for us. We were congratulating ourselves for having made that decision, since both of us have been working from home for over a year now. If we had still had a car, all it would have done for us was eat money. Have you thought about that much? That unless you are a ride share driver, your vehicle probably sits around uselessly 90% of the time? It seems that a lot of people feel panicky when they think about getting rid of a vehicle. The idea makes them feel trapped and poor. I get it, but it still seems weird to me. Driving is incredibly stressful. It’s also expensive. I first decided to get rid of my own car when I crunched the numbers and suddenly realized that my car cost a quarter of my net income. A QUARTER! Granted, I didn’t make very much money. From my perspective that made it even more important to cut that thing loose. Car, I cannot afford you. I sold my vehicle, quit having to make car payments or cover insurance, and within a couple months I realized how financially freeing it was. Suddenly my credit cards were paid off. I bought a new couch and went on a proper vacation for the first time. Then I married someone who still had a vehicle. In a way it was cheating. I had access to his truck if I wanted to do something complicated like go to Costco. I kept most aspects of my personal car-free lifestyle, like riding the bus to work. A few years went by, and my husband got a job with a very gnarly freeway commute, and he kept getting delayed by construction or accidents, and sometimes we couldn’t have dinner until almost 9 pm, and we both got tired of it. We decided to move and just make sure we lived within walking distance of his work. This was the “reconsidering” phase of our marriage. We moved to a walkable neighborhood, and we loved it! Suddenly, instead of these nights of nightmare traffic, there were quiet evening strolls past various rose gardens and fruit trees. It was like waking up in a movie with a happy ending. When it was time to relocate again, we took it a step further. If we were going to stay in a walkable neighborhood in our new city, it meant living in a smaller space. We got rid of the majority of our stuff and went for it. Would we go back to the way we lived when we first got married, when we had constant access to a personal automobile and plenty of consumer items? No. Even though it meant having two bathrooms. There are some considerations coming up for us. It’s possible that we might have to start going to work in person, probably not full-time, but maybe more often than zero. What are we going to do? We talked about buying a car again. We can afford it - we’re debt-free with plenty of savings, partly because a car is no longer eating $700 a month of our income. It would make certain parts of life more convenient, of course. If it was all “lose” and no “win” then nobody would have one. The reason we decided not to, even though we both work in the same place, is that it would add significant complications to our lives five days a week. Every morning, we would commute in together - unless my husband is on travel, which is often and also wildly unpredictable. Either he would constantly feel like he was wasting his life going in late and staying late, or I would be exhausted from trying to start work with him at 7 am. Either way we would both be chafing at each other. Not only is he an extreme lark, he’s also deeply punctual, while I am dopey in the morning and incapable of being hurried. So a car would ruin our mornings and probably cause us to start the day annoyed with each other. Then there would be the daily complication of whether we were leaving together or not. Did one of us have a late meeting? Did he need to go straight to the airport? Was one or the other of us invited out to dinner with coworkers? Was he trying to hit the gym? We realized that would be our situation. If we bought a car, we would have to check in with each other literally twice a day to figure out if we were riding together or not. Very messy. Some people may be recognizing themselves in this. Others might be shaking their heads, thinking, yes, this is exactly why we have two cars. I will never give up my car because I can’t stand to be in that situation. If that is the case, I would suggest a quick, cursory check-in. Are ya debt-free? Do ya have plenty of savings? No? Okay then how much do your cars cost again?? We won’t buy a car again. It’s stressful and we’re over it. What will probably happen is that if I get called in, learning that I am expected to work on-site, I will either ride the bus and wear my MicroClimate helmet, or I might buy an electric bike. (Nowhere really safe to park it in our current apartment, though). My hubby might buy a motorcycle, not so much for the commute as for the fact that he just really loves motorcycles. It’s also possible that we might just find ourselves a place a couple miles closer to work. Who knows? Nobody has to do anything. Reading this post certainly will not force your hand. It can’t hurt, though, to occasionally ask yourself a few strategic questions about your lifestyle and whether it really is working for you as well as you think it is. Wouldn’t it be interesting if you made a few changes, saved a bunch of money, and also had a more satisfying and interesting commute? I saw something funny the other day. I got into a rideshare vehicle, and the driver had something hanging from his rearview mirror. It was: a Bitcoin.

Or rather, it was a gold-colored token or medallion in the shape of a Bitcoin icon. A “real” coin made to look like a virtual coin. How marvelous! I couldn’t take my eyes off it. This solid Bitcoin was one of the single most hilarious and interesting things I’ve ever seen. What was it saying? I couldn’t really ask this driver because he had a plexiglass divider installed between the front and back seats. Between that, both our masks, and my face shield, there wasn’t much point in idle conversation. What was it saying?? Payment accepted in Bitcoin? I heart Bitcoin? Wish I had some Bitcoin? Buy me a coffee and I will explain the blockchain to you? Bitcoin bought this car? If I had a Bitcoin mining rig I wouldn’t have to drive a rideshare vehicle during a global pandemic? I liked that solid Bitcoin so much I considered trying to buy one for myself as a joke. But then if anyone else saw it, they’d probably insist on talking about Bitcoin with me. I’m not necessarily against the idea - of Bitcoin itself, mind you, not of inviting bros to lecture me about it. In fact I’ve decided to charge for that. I’m available to debate you on any subject for $10,000 an hour, and I’ll let you rant at me without responding for $25k. Why not. A girl’s gotta eat. Will I take payment in Bitcoin? No. I think it’s the currency of the future. That or something like it. It stands to reason that all the space colonies will take either some kind of digital payment, or scrip, whether that’s at the “company store” or whether it’s some kind of provisional territory currency. Marsbucks or Lunacoin. Perhaps it will be more along the lines of an automatic debit to an account, such that the user is barely aware of the balance. In space there probably isn’t much to buy. It was a strange day in rideshare world, because the Bitcoin driver dropped us off, and another financially-oriented driver picked us up an hour later. “We” would be myself and my little gray parrot Noelle, who exists in a cash-free world of total abundance. People just come over and hand her radishes and lettuce and turn on various music playlists and build her forts, and she shrugs and enjoys. As far as she is concerned, even your shoes belong to her, so why should she apologize for destroying your shoelace tips? Wealth is whatever you think it is. Our return driver described himself as a trader. “A day trader?” I asked, partly out of politeness and partly because it seemed amusing to me. Perhaps he would show me the setup he used to make trades between drop-offs. He explained that he is not a day trader because he keeps most of his stocks for as long as ten days. “I measure time in ten minutes, ten hours, and ten days,” he told me. I’m an investor, too, I offered. What’s your biggest return? he asked. Well, I bought Tesla at $42... Yes, but over what span of time? he asked. Okay, that’s a good one. I’ve made, depending on the week, about 1500% interest on that one purchase. But he’s right, it did take me longer than ten days. What is most instructive about this conversation is the context. Here we are, driving up the road, one rideshare driver in the front and one middle-aged office professional in the back. Both thinking that we have any inkling of finance or macroeconomic trends. Meanwhile passing through one of the most expensive zip codes in Southern California, a place where the dog walkers probably out-earn both of us. It hasn’t escaped my notice that so many rideshare drivers have vocal opinions about the stock market, or cryptocurrency, or various entrepreneurial ventures, or real estate. With a low bar to entry, people show up from a wide variety of backgrounds with a broad spectrum of goals. I try to collect tips from them to pass on to other drivers. For instance, I was talking to a kid with an interest in real estate investing. I pointed out that if I drove as much as he did, I’d be taking notes on the neighborhoods I passed through and checking out comps. “That’s a great idea,” he said, seeming surprised. I told him the other thing I would do is try to pick the brains of his passengers. I told this driver - a Russian immigrant who has lived in a dozen cities - that I’d met another driver who traveled from state to state, driving to pay her expenses. Seems fun. The reason my driver was so interested in the stock market is that, he told me, under communism, anyone who tried to buy stocks would go to jail. Wow! He came here 17 years ago because he was so interested in the workings of capitalism. Under communism, no jazz either, he said. I wondered what these two drivers would have to talk about if they met, which is unlikely to happen since they are both drivers. Crypto or stonks? Both? How much of each? I’d love to be a fly on the wall for that conversation. I like to be aware of what’s going on in pop culture. I also consider the chatter of random people such as cab drivers, baristas, and hairdressers to be a strong indicator of trends. One of those is investing. When almost any person of almost any professional background starts expounding on the virtues of a particular investment vehicle, it’s probably getting kinda overvalued. You think? If you care for the opinion of a random blogger such as myself, I’ve got all my new money in cash, waiting for the downturn. Eleven years of a bull market, I ask of you. Am I putting any of my money in Bitcoin? Call me when the transaction costs are down to a dollar and we’ll talk. My friend makes $1000 to $2000 a month dog-sitting. Can you believe it?

I thought I would share this story, partly because we’re thinking of trying what she is doing, but mostly because it is so illustrative of the fact that there are infinite ways to bring in money. It isn’t really the cash that motivates my friend. It’s the dogs. Say there is someone who absolutely adores dogs. Loves dog energy. Thinks that dogs are the best creatures on Earth. Is a total “animal person.” Now, imagine that same person loves to travel, both for business and for pleasure. Is not in a position to own a pet. Does not have immediate plans to settle down. What would be a way for this dog-loving person to have a dog around as often as possible, while not abdicating on a commitment? This is where the dog-sitting idea came in. Why not be surrounded by dogs on demand, and also get paid for it?? It’s now easy to sign up with one of several pet-sitting apps. It doesn’t take long in a reputation-based business like that for individuals to stand out one way or the other. My friend is a business professional with an immaculate home. She lives alone, doesn’t smoke, and has no other pets. Those qualities are true of some people and not of others. I know from experience the way my friend spoils dogs. Our own dog used to try to jump in her car window whenever he saw her. We came home from a week overseas, and he didn’t even meet us at the door. He just popped his head up and stayed in her lap. Oh, I see how it is! Who is the real winner of this arrangement? The spoiled dog? The dog-loving lady who isn’t ready to commit? Or the traveling couple who worry so much when they are out of town? Answer: Everyone Everyone is the winner in this scenario. We’ve been thinking of ways to expand the services she offers, without of course going to great lengths of effort or expense. Dropping dogs off at the groomer’s before the owner comes home? Taking dogs to their vet appointments? Anyone who travels a lot for work would probably be thrilled to be able to hire this out. Find out the going rate, shrug, and pay it. Personally I think ‘dog massage’ would be another winner. For someone who is willing to give a dog massage, and for the right breed, that seems like it could be a natural fit. I used to live next door to a huge elderly Newfie who probably would have loved it. Another way my friend could make more money with her current dog hustle would be to set out on her own and book her own clients. She wouldn’t have to pay a cut to the app any more. Another thing she could do would be to reach out to local dog walkers, veterinarians, or groomers and offer her card. Not everyone is willing to host dogs overnight; not everyone lives in a place that would accommodate it. We in our fifth floor apartment would not be able to do this sort of business right now, especially since we work office jobs at home. Barking would not be a value-add for our video meetings. There are probably a lot of people who live in an ordinary suburban house who also enjoy having dogs around. Just as there are probably a lot of people who have the space to rent out a room on AirBnB if they cleaned up and got rid of a few truckloads of clutter. The bar to entry for certain side hustles is lower than it’s ever been. A lot of people are overlooking an asset in their life, either because they have always taken it for granted or because it has never occurred to them that it’s an asset. Others are in a beaten-down and depressive state, convinced that they are no good to anybody, when the very next day they could quite easily be making someone’s life easier or better. What are your assets? A garage - even if it’s currently packed wall to ceiling A yard - even if it’s overgrown and full of junk More than one bedroom - even if the house is hoarded hip deep Talent with animals Decent internet connectivity, which not all neighborhoods have A smartphone A working computer of whatever age Literacy Ability to pass a background check Ability to pass a drug screen A high school diploma - or not - plenty of people have a GED I hadn’t had a day job in over ten years when I applied for my current position. I said as much in my phone screen. They still made me an offer. It is right and good for the employer to decide which candidates they want, and far be it from me to talk them out of it. Could my friend be doing something else with her time to make an average of a thousand dollars a month? Or more? Probably. Do her clients care? Probably not. The dogs certainly don’t. Wherever we live next, when the pandemic is over, we might very well sign up as dog-sitters. For the money? No, not really, although it’s fair to charge when we might have reason to replace our sofa. We would do it because it’s nice to have a dog around, and also it’s challenging to be a pet owner with a busy travel schedule. How about you? Would you consider something like dog-sitting to make some extra money? Do you have a favorite thing that could potentially be a source of income as well?  $6 plant in continuous bloom for four months A lifestyle upgrade is anything that makes your life better, easier, more comfortable, more interesting, more fun - or anything else that you decide is an improvement over whatever you had before.

This idea totally turned around how I think about my New Year’s planning. When other people hear ‘resolution’ they tend to think of something like “quit biting your nails.” I think “lifestyle upgrade.” What am I going to do next year that will be better than what I did this year? Lifestyle upgrades can come in many forms. You can get rid of an annoyance, and that will be a lifestyle upgrade. You can change something you’re doing, even in a small way, and that could be a lifestyle upgrade. You can replace an object or rearrange a room, and that could be a lifestyle upgrade. You can learn to do something new, and that might be a lifestyle upgrade. You can make a new friend, and that would most likely be a fantastic lifestyle upgrade. It’s possible you could spend money and buy something that might be a lifestyle upgrade - but most of the best ones don’t cost anything at all. Some lifestyle upgrades can actually come from spending less money than you were before. (An example of that might be learning to make better coffee at home instead of paying more for a to-go cup). (But then again, if it streamlined your morning, spending more for the to-go cup each day might be the real upgrade). The most important feature of a lifestyle upgrade is that it improves *your* life. It’s not necessarily something trendy that works for other people. It’s not something you do in service to someone else, unless you truly thrive on that and it ripples back to you in some way. A lifestyle upgrade is not something you feel like you “should” do to get an A+ on your report card. The way you know you’ve hit upon a lifestyle upgrade is that you just really dig it. It becomes a habit almost immediately, because you realize you like it so much better than what you were doing before. An example would be throwing away your old flat brown pillow and replacing it with a new one that fits you exactly right. If lifestyle upgrades cost anything at all, it’s funny how often it’s under $10. Like a new kitchen sponge. I like focusing on lifestyle upgrades, because it’s the most upbeat and fastest way to demonstrate the value of doing an annual review, planning, and making resolutions. These are some of the lifestyle upgrades that my hubby and I implemented in 2020. We decided to only watch movies if they rated at least 70% on Rotten Tomatoes. There were just too many occasions when we watched something with a good preview, and it turned out to make no sense or have giant plot holes. Then it would turn out that this great movie we had been so excited about only rated a 55%. It is crazy how much of a lifestyle upgrade it is to quit watching lame movies. We also decided to watch a documentary once a week. Usually the documentary is both funnier and more interesting than whatever fictional film we’ve chosen. Documentaries are usually also short. I learned to cut my hubby’s hair, and then I learned to cut my own. Surprisingly satisfying. We switched to a new boarder for my little gray parrot. They’re closer, better organized, nicer, cleaner, and they do a better job on grooming. My bird is much less stressed when she goes over there. I think they’re also maybe a dollar cheaper. We gave away a bunch of stuff, including two tables, a box of wooden hangers, some books for the Little Free Library, and a distressed plant. We rearranged the stuff on our tiny balcony and put up a planter and a hummingbird feeder. (Anniversary gift). This completely transformed, not just the outside space, but our living room too. Now we get three species of hummingbirds and four other species of passerines coming by from sunrise to sunset. We started using a humidifier next to the bed at night. Almost instantaneously we both stopped having sneezing fits. It’s hard to say whether it was the dry air, distant wildfire smoke, or smog, but we hadn’t realized how bad it had gotten until it went away. I moved our whiteboard to the hallway and hung it on the wall, instead of having it stand on a bookcase. It looks better where it is, it’s easier to use, and the space where it used to be looks much better without it. Moving it took a total of 15 minutes. I rearranged the cabinets under the kitchen sink and the bathroom sink, the linen closet, and the fridge. Same space, same dinky apartment, totally new satisfaction when looking for stuff that is now easy to find. We started getting produce delivered again, through the same service we’ve used off and on for ten years. Better for the farm, marginally less expensive, and it cuts our grocery trips in half. Hopefully that is safer for the grocery clerks, the delivery driver, our community - and us, of course. We built Noelie a cardboard box fort. It started as one box, then two, then three. Now it’s four stories high and has six “rooms.” This has been a massive lifestyle upgrade for her, but also for us. It’s stupidly entertaining and it takes little more than assessing boxes while we sort the recycling. We started going to a local park on the weekend when the weather is nice enough. This park is big enough that we can pick a spot to sit away from the paths, and nobody comes within thirty feet of us. It’s about a three-mile round trip. Hanging out there helps us feel like we got out and did something, and helps avoid the feeling that the walls are closing in. Since we started doing these walks, we’ve seen a few hawks, a coyote, and an owl. We decided to stretch out our holiday meals and only cook a couple of dishes each night, rather than spend all day trying to replicate a buffet. Magic. We are definitely doing it this way forevermore. I got a job! My first formal day job in over ten years. I knew I would want, no, NEED something to do during isolation, which I thought might last three years. It would give me a social outlet too. It has felt great to be back in the game, I’ve made friends, and it’s psychologically really meaningful to me to have life insurance on myself. I’m very busy and often pretty tired, but overall, getting a new job has probably been the biggest lifestyle upgrade of them all. Notice that almost everything we did as a lifestyle upgrade is free of charge. A couple of things wound up saving us money, like going to the park on weekends instead of the movie theater. (Although that is a side effect of the same 2020 that everyone else has been having). The few things we bought, like the hummingbird feeder and the humidifier, can be purchased for under ten bucks). Part of my New Year’s planning is to think of more lifestyle upgrades for the upcoming year. What lifestyle upgrades are you going to make?  Past Jefferson talking to Future Jefferson Don’t worry, I’m not putting actual financial numbers out there!

The most important thing I could probably say right now is, remember April You? The version of you that is in a blind panic over the deadline to file your taxes? Right now you have an opportunity to send that Future You a very thoughtful gift. You can start getting organized now, a little bit at a time, and then April 15 You can maybe go for a walk and watch the sunset. That never works, though. There is nobody we will ever treat as cruelly as Future Myself. I like to take a little time every December to imagine Future Me of different ages and ask what she is doing with her time. I like to imagine that she is comfortable, that all she really has to do is eat her oatmeal and do cryptograms all day. I would never want her to worry as much about money as Young Us did, because Young Us could go to work to earn more, but Old Us probably can’t. Let’s face it, unless you’re already 80, it’s easier to earn money now than it will be then. This is why it’s helpful to do a financial review. If not in December, then when? Seriously. Pick a month. Draw a month out of a hat so it’s different every year, if that’s what it takes. I was poor until I was 30, and going over my finances used to make me cry. It basically went like this: Bills: Yes Savings: No Retirement: *scoff* There was a time in my life when my rent was 80% of my income. And I had roommates. It was only by keeping a keen eye on my (lack of) money that I started to be able to make changes. I would read personal finance books, and there were not just chapters but entire sections that applied to financial vehicles I did not have. I didn’t have a 401(k) because my job didn’t offer one. I didn’t have an IRA because I didn’t have enough saved to open an account. I tried to have a savings account but I kept having to use it (all) to pay bills. There was also a time when I had no credit score because I had no credit. Credit cards used to be hard to get. I had a store offer to set me up with a store credit card, and the clerk was telling me all about how single moms with no job could get one. I was declined. When I finally managed to get a credit card, my limit was $250. It was still $500 when I turned 30. Although, pro tip here - credit doesn’t matter if you don’t use it. If you never carry a balance it doesn’t matter what your credit limit is, and it also doesn’t matter what your percent interest is. When I was young, working as an office temp, sometimes I could only think about one week at a time. I might have an assignment that only lasted a day, and then I’d have to get another assignment. My commute was all over the place. I didn’t have a car, nor could I imagine having to buy gas. I would ride the city bus, sometimes two hours each way for a job that might only last three days. It was a mess. I had no debt, but I had nothing else either. No savings, usually no more than $30 in my checking account, usually not enough change in my pocket to use a phone booth. My roommate kept stealing my laundry quarters. How could I do a financial review? The answer was the same, for years: Try not to get overdrawn. I knew it would help if I earned more, but I didn’t know how to find a better-paying job. I didn’t know what I wanted to do or how to get credentials. It didn’t help that I looked young for my age, and I could pass for a teenager into my early 30s. It’s different now! 99% of my thoughts about money used to be not thoughts, but feelings. Dread, anxiety, panic, stress, irritation. There wasn’t much room for much else. What goes where the stress about bills and debt used to go? We’ve been living on half our income, or less, for years. We’ve been debt-free for years. We probably have six months’ living expenses saved up - possibly more - but why bother counting it out? When in doubt, shrug and save more. We’ve maxed out our retirement funds at work. Did you know there’s actually a maximum amount that they let you save? Everything is automated. Each week, money is deducted and put into our 401(k)s and set aside for our IRAs, and we only have to think about it when we move the IRA money at tax time. All our bills are automated. We are big users of reward points, so we put all our expenses through our credit cards, but we pay off whatever balance week by week. It is hard to overstate what a major emotional difference it makes to be debt-free and have a high savings rate. On one side of the divide is an ocean of tears with thunderstorms of splitting headaches. On the other side, it’s just... mild and sunny. We never argue about money because what is there to argue about? I don’t want to brag. That is not why I’m sharing this. I want to bring hope to other people who are as flat broke as I was all those years. It is possible to get out. It is possible to move past it completely and just never feel that way again. It takes focus, though. Once a year is a good start, although monthly is better, and weekly is even better when things are really tough. Make a list of every account you have. If you forget some, that’s okay, just add them as you run across them. Or set up a financial tracking app, if you’re brave. Total up everything you owe and everything you have. Start putting together an estimate of your monthly expenses, plus the weird quarterly and annual ones like car insurance. Find a book or a podcast or a website or a radio show or a friend that will teach you basic personal finance skills. If you didn’t get a personal finance class in high school, shrug it off, because that information is wasted on teenagers anyway. You can learn today. Maybe start with a search for “financial independence retire early” and see what you find. Our way is a radical way. We decided to live on half our income and save the rest. We got rid of over 80% of our stuff, and we live in about 1/4 the space we had when we were newlyweds. We haven’t had a car in nearly four years. Literally anyone can do what we did, which is to cut expenses, live in a small apartment, and not own a car. It sounds shocking, until you try it and realize that it’s not a big deal at all. Maybe once a year, pull back and spend a day thinking about where your money goes, where it comes from, and what things might be like if you made some changes. Maybe even radical changes?  Talking about money is why my husband and I are married. Done right, a big money talk can be exciting and fun.

Then, of course, there’s the way most people do it. When you’re broke, which we both were when we met, thinking about money is stressful. It makes some people cry, others freeze up, and others want to throw things at the wall. It doesn’t have to be that way. The trouble is, most people don't know that. All we have to go on are the examples we learned in childhood, the sanitized academic exercises we might have learned in one semester of personal finance, what we see in the media, and maybe what we’re being pitched by someone or other in an MLM scheme. (I have one of them in my life *again* - sending me texts and emails over the holiday weekend asking me to pitch her company’s product to my work, which is a non-profit - and probably quite cheesed off that I am ignoring her). (Come to think of it, I’m probably going to have to have a sort of big money talk with her, too). Fear of conflict is what holds so many of us back. We won’t take the initiative because we don’t really know how to do it, how to open up a conversation about a topic that is so loaded. Go first. That’s the first rule. Be willing to take the lead, be willing to be the planner and the researcher. One way or the other, there is no escape - you must take total responsibility for your own finances whether you are alone or whether you have a partner. It might not work. People often need to be told that they don’t need permission to break up, that their relationship might not be viable and that they might need to get out before doing anything else. Your partner might be completely unwilling to make changes in this area, and that’s okay. You’re not the boss of them and they aren’t the boss of you. All right. Assume that you do have a partner, which is why you would need to have a money talk, and that you are fairly sure your partner is willing to hear you out. What you’re aiming for is a high-level strategy, not something like “I can’t believe you spend $5 a day on chewing gum.” (True story). Or, “You have to quit buying so many Funko Pops or we’ll never be able to go on vacation.” Your motivating force may be irritation with your partner’s spending habits, and if so, I don’t blame you - but it also means you’re losing the game. The truth is, at a certain income level, an “excessive” spending habit is actually affordable, or even negligible. The big money talk, on a strategic level, is about two things. It’s about lifestyle upgrades and it’s about personal empowerment. The first is about what sort of stuff you would buy or what you would do in your spare time, if you could “afford” it. The second is about whether you both actually enjoy your jobs and find them interesting versus feeling constant stress, burnout, and background dread. Getting rid of debt is both a lifestyle upgrade and a personal empowerment. Talking about the debt first doesn’t really work. Generally it will make anyone flinch and start feeling defensive. The entire concept of debt revolves around guilt, blame, and shame. You can skirt right around that by talking about blue-sky visions first. This is where you have to do a lot of prep work before you initiate the talk. What do you personally want? What would you do differently if you were debt-free? What would you do differently if you had $100,000 in the bank? These are the types of questions that get the juices flowing. These are the types of questions that encourage your partner to actually want to engage with the discussion. In my coaching work, I have discovered that almost nobody has an answer to the question, “What do you really want?” Most people can’t finish the “perfect day” exercise, either. We don’t know what to do with ourselves when we aren’t fussing and fretting over something. It’s so, so important though! Most of the items in my perfect day/dream life don’t cost money. They include lots of time in nature, staying in touch with my family, eating a hot breakfast on weekend days, and reading a lot. It’s possible to do all of those things regardless of one’s income or balance sheet. This is another area you can explore with your partner, to wit, “What do you already know makes you feel wealthy?” The goal of the big money talk is to figure out how you can facilitate each other in whatever you both need to live a bigger life. There are two ways to do it, the trapped way or the liberating way. Either you feel like you’re pinching every penny until the end of time, or you feel optimistic and lit up because you know you’re making steady progress. Our first big money talk happened not long before my husband proposed. The way I remember it, he spontaneously offered to come over and do a ten-year financial plan together. The way he remembers it, I suggested it and asked him to show me how he did his. Somehow we both think it was the other’s idea. It was fun. That evening is probably why we finally did get married. This year, we realized we had hit the target right on schedule - in fact, we were .1% over our goal. If you want to start this type of discussion with your partner, you can start with any introductory personal finance book. Or you can start by introducing the concept of FIRE, financial independence/retire early. (We don’t plan to retire early because neither of us plans to retire at all). Start by asking what your partner would really like to do, and offer to facilitate that in some way. Make sure you can both explore the topic with curiosity and willingness. If you’re going to be a strong team, this big money talk is going to go on for years or decades, so make it easy to agree with you.  My plans Black Friday has another name, and that is Buy Nothing Day. For the past several years, that is how I’ve chosen to celebrate. This year, 2020, it seems there is even more reason to do it than normal.

I went out to shop on Black Friday precisely once. I set an alarm and got up to go shopping with my brother and his family. I am not an early bird, and I was a poor student at the time, but I had set my cap for one particular item and I was pretty excited that it would be on sale. I didn’t understand how this stuff worked, though. Black Friday didn’t mean that every single item was discounted. I went straight to the aisle where my prize was - I believe it was a buckwheat pillow - only to find that it wasn’t on sale. Then I spent the next two hours trudging along and yawning while my fam bought a bunch of socks. All that and I Bought Nothing after all. I will forever associate shopping on Black Friday with long lines, surly throngs, and people honking at each other as they endlessly circle parking lots. For what? This year, there is no way in hell that I would physically go to any store on Black Friday, not anywhere on Planet Earth. I wouldn’t go out even if it meant I got a coupon for a hundred thousand dollars and a free hot chocolate. BTW you did know that hundreds of people around the world have caught COVID-19 twice, right? You know there’s no immunity and you can get it twice? Okay, just checking. I guess a lot of people buy stuff online, and I’m not planning to do that either. There are a lot of reasons why I’m into Buy Nothing Day. More keep getting added to the list every year. Right now the main one is that, this year, the search for bargains is going to put thousands of people in the hospital and a lot of them are going to die within days. Usually, it’s not nearly so compelling. I always found the concept of a holiday that drags out over two months or more to be confusing at best. Why that one? Since I plan events for the morale committee at work, I’ve put more thought into these things than I usually would. Holidays can be divided into the ones for food, the ones for dancing, the ones for candy, and the ones for gifts. Halloween and New Year’s are the ones for dancing, Thanksgiving and Fourth of July are for food, for example, and Valentine’s Day is for candy. Christmas is the one for shopping, and that’s why there’s this rabid, intense pressure to decorate everything, pump perky music through every pipe, and sell, SELL, $ELL!!! I can’t bear it. Everything about this season sets my teeth on edge, from the green and red color scheme to the tinsel and lights to, most especially, the music. It starts earlier every year, and every year, I flinch and head back inside for my annual holiday sabbatical a little earlier. This time, the store across the street from our apartment put up huge inflatable Christmas decorations the first week of November. Now, on the rare occasions when I leave our building, they are literally the first thing I see. It’s hard to escape the festive frenzy, though I do try. Obviously not everyone feels the way I do about the holiday that never ends - I’ve noted decorations still up well into the second week of February, and they start showing up in October, so somebody must be into it. Does it have to be about shopping and buying and purchasing and spending, though? What I usually do on the day after Thanksgiving is to hang around with my family, telling stories, cooking together, and playing games. That’s what makes it feel like a holiday to me. There aren’t really any other four-day weekends when I get to be with my family and just hang around. We live a thousand miles apart, and it’s a pretty big deal for us all to be together. This year, of course, I’m not going anywhere near the airport, nor would I spend two days driving each way just to put myself, my family, and everyone along the I-5 corridor at risk. It’s irresponsible and, frankly, unpatriotic to travel from a hot zone to a less-affected area during a pandemic. I just read that 1 in 3 parents (in the US, obviously) feel it’s worth the risk to have a family gathering for Thanksgiving. There seems to be this logic either that “we’re too smart and cute for bad things to ever happen to us” or that “this might be our last chance to see each other.” As for the first, I won’t comment, but as for the second, let’s not make it a self-fulfilling prophecy, okay? This year we’re going to hang out on Zoom, which everyone is probably fed up with by now, but we are all familiar enough with it that we can play games and gossip just the same. There is the added advantage that all our pets can attend, since they’re in different rooms. Maybe this will be the holiday season when I don’t gain several pounds between Thanksgiving and the New Year. As far as buying things and keeping the economy going, I think that this artificial seasonality and the social pressure to buy tons of gifts for all and sundry, I think maybe it’s better not to plan the entire year’s revenue targets around that. What would an economy look like if it was not a December-oriented consumer economy? After all these years, I am firmly committed. Celebrating Buy Nothing Day instead of Black Friday means I get to lounge around in my pajamas, reading, maybe taking a nap, talking to my family and playing some games. The alternatives are driving in circles around a bunch of parking lots, standing in line with cranky people, and, this year, maybe picking up a lethal disease. Count me out. Care to join me? The relaxation and debt-free part, that is.  Almost everything visible in the van is out of our lives now *shrug* This is not the first time this has happened by any means, but I recently had a conversation with someone who had stuff in a storage unit for ten years.

You already know what I’m going to say about this. What in the Sam Hill could possibly be valuable enough to keep it for ten years without using it?? Stuff sits in storage mostly out of inertia. Out of sight, out of mind. Many people probably feel that it’s worth paying the rent every month simply for the luxury of not having to expend effort to deal with the situation. When is it ever a good time to get a truck, spend half a day clearing out a storage unit, and then figuring out what to do with all that stuff? Since I talk to people about clutter all the time, I do get to hear these stories occasionally. Sometimes, yes, people do get tired of paying money for nothing and they go and clear out their storage units. (Yes, it’s not uncommon for someone to have two separate units, although most people can’t afford three). What do they do with the stuff? Move it into a garage, shed, or “spare” room! It’s almost unheard of for people to get rid of all of it, to just say, You know what? I haven’t missed any of this stuff, I’ma go drop it off. If you do have a storage unit, at least know that you’re not alone. There’s a reason why it’s so easy to find storage units in the US - it’s a multi-billion dollar industry. (I literally just mis-typed that as “in dusty”!) Having a storage unit doesn’t particularly have a cost in terms of mental bandwidth. Probably a lot of people continue to pay that bill and almost never think about what items are actually in there. That’s the whole point. Most people do not like to make decisions. The cost of indecision, here, is a financial one. I did the math with one of my friends, several years ago, and she had spent TEN THOUSAND DOLLARS on her storage unit. I am not kidding. Do you have an extra $10,000? I don’t. This is where we take a moment to talk about the difference between an “asset” and a “liability.” An asset has value and generates value. A liability costs money. It’s hard to come up with something that is truly an asset, because there are so many misconceptions here. A lot of things that seem to be assets are actually liabilities. Understanding the difference can be like flipping a light switch in the perception of one’s household finances. A toolbox. We’ll go with that. If you use tools at your job every day, then those tools are helping earn your paycheck. At a certain point, their cost was fully amortized, maybe even the first week. I cut my husband’s hair today, for the third time ever, and that was when the clippers and scissors I bought paid themselves off. We would have spent more at the barber for three haircuts than what the equipment cost. Now those clippers are an asset that can save us about $100 a year. If we had a storage unit, the clippers would not be in storage, because it would be too annoying to go dig them out every time my man started complaining about his bangs getting too long. If we had a storage unit, we would have two options: One near us at $250 a month, or one across town at $150 a month. I know because I looked into it when we were first planning to move here and debating whether we should really get rid of 80% of our stuff. This means we would have spent either $3000 a year for a unit we could actually get into, or $1800 a year for one that would have required us to either get a car, pay for a rideshare, commute farther to work so we could be near the cheaper storage, or pester other people to give us rides to go get random stuff when we needed it. Or of course pay $1800 a year - the cost of a mighty fine vacation, by the way - just to ignore all that stuff we weren’t using. Now let’s multiply that by five years, and we get: $15,000 OR $9,000 + externalities. Let’s game this out and try to come up with what kinds of possessions it would actually be worth more than $9,000 to store. Business equipment! If we were professional landscapers or event planners, for example, our expensive storage unit could actually help us to earn money. In fact the facility we used for a month when we moved was full of units like that, for professional contractors, painters, landscapers, and others who, like us, would be hard pressed to find a house with a garage out here. We aren’t, though. We don’t own a business. Like most people, what we would have kept in that unit would have been stuff we didn’t have time to deal with during the move, or stuff we felt was Worth Something (TM), and we wouldn’t have realized that five years were going to go by without us making a decision. But storage doesn’t cost that much where we live, you say. Sure, okay, but then what is your exit strategy? Have you sat down and opened the calculator app on your phone and figured out what you have already paid on this liability that is your storage unit? Oh, but it’s not actually my unit, you say. It’s actually So-and-So’s. I know for a fact that other people love to spend their money helping me solve my problems! (Or not, cough) I’m willing to venture that a lot of storage units have stuff belonging to more than one person, and that is part of why nobody has said, I am no longer going to pay this bill. I’ve heard of parents paying for kids’ storage, siblings storing each other’s stuff, and of course people getting stuck with things that belong to an ex, or an old roommate. There are a lot of “watch my dining table for me while I”... have no intention of ever dealing with it. Whose dining table is worth $9,000 anyway? If your parents are storing your stuff - think about whether they’re going to be able to make ends meet on a fixed income. Would you rather they pay for your storage if it meant they have to come live with you when they turn 80? If anyone else is storing your stuff, pull up your socks and go deal with it. If you’re storing someone else’s stuff, this might be a good moment to ask yourself whether this is what is holding you back. You can go over to your unit, look it all over, and take care of your own stuff, then call that person and tell them it’s time to make arrangements with the storage company. Chances are greater than 1% that they will decide it isn’t worth their bother. We did the seemingly impossible. We gave away or sold 80% of our stuff when we decided to take the dream job and move to the beach. Looking back, we made so little at our one-day garage sale that we wish we had simply donated everything and spent that day relaxing. Have we missed any of the stuff we got rid of, like our ladder and our wheelbarrow? Nope. Could we go to Home Depot with the thousands of dollars we saved on not having a storage unit and replace all of it? Yes, and then some! Like most people, what we would have spent on a storage unit over five years would be more than all our furniture and wardrobes combined are worth. Do you have a storage unit? Why? What the heck is in there? Why are you keeping it? When do you think you will actually use it again? Have you decided yet? How much is that indecision costing you?  Walking by someone’s apartment complex We’re thinking about saving up for a house. This is more interesting than it probably sounds, because where we live, even a very ordinary house is stupidly expensive.

How ordinary? How expensive? Picture a 1200-square-foot house with a tiny yard and no garage. This modest house has not been remodeled in at least a decade, has a tiny kitchen and a tiny bathroom, has almost no storage, and can best be described as “funky.” If you’re lucky enough to find a house like this in our zip code, it’s going to cost significantly more than our entire retirement portfolio. We can actually qualify for a mortgage in our area, because we’re middle-aged and we have great credit. But that mortgage would get us a condo or townhouse, not a house-house. Not something with its own yard. We did it to ourselves. We chose to live in an area where even our boss’s boss can’t afford to own a house. Our colleagues either live in tiny apartments just like ours, or they commute, in many cases over 90 minutes each way. We know more than one person who lives in an entire different region over four hours’ drive away and only goes “home” on weekends and holidays. There are multiple van pools. It’s a California problem, to face paying quadruple for the same house almost anywhere else. It’s a beach community problem, to face a real estate base that is shabby and crumbling because it’s been a seller’s market for over a hundred years. We’ll be on a walk, see a house for sale, and check the listings just out of curiosity. Then we will stand there with our mouths hanging open because of the sheer temerity of asking two million dollars for a heap like that. I can see the future, and it’s a future with a lot of plaster dust and mallets. I come from a family that is constantly remodeling something, anything, somewhere, somehow. At least one of us has had a project underway since 1990 and it’s never stopped. I’m quite good with tools for someone who usually has a book in my hand. Then I went and married a tool man who loves gardening. This is what’s going to happen. We’re going to wind up remodeling a house together, because it’s our destiny and there is no escape. Then we’re going to drive each other crazy with it, because remodeling is hell. Then, as soon as we “finish,” we’re going to have another project in mind. Once it’s started, it’s like a tractor beam, dragging you towards it with galactic force. This is where strategy comes in. There are only a few ways for someone to buy a house in our area.

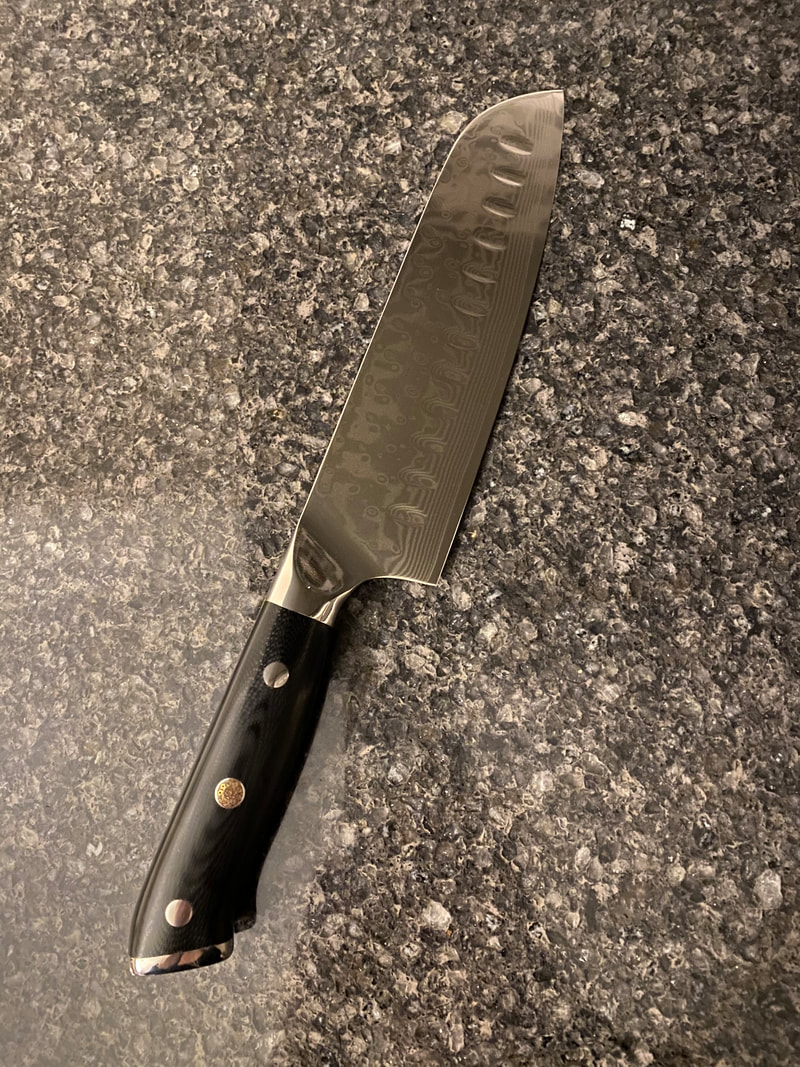

It’s like this. If I sold a screenplay for two million dollars, after taxes, I could put down what was left on a house here. And *then* we could qualify for a mortgage on the balance. That’s the bar. Where we are right now, our entire combined annual gross income wouldn’t be enough for the down payment on the kind of house we would like to buy. Oh, wait. There actually is another strategy we could use. That would be to give up on the impossible dream of buying a fancy-pants beach house in a foo-foo beach community. If we just let it go, we could save toward a realistic, modest house almost anywhere else in the world and then retire there quite comfortably. Where’s the fun in that, though? What we’ve learned from downsizing over the past several years is that we can do it, yes, and we have enjoyed the results in most ways. Taking the financial pressure out of our marriage has been wonderful. We’ve also eliminated entirely the stresses that most families face - almost all of them - including commuting, yard maintenance, and most housework. We don’t even have carpet to clean. Where we are right now, we’re on track to be able to retire. (Although neither of us really believes in traditional retirement, because sitting around with nothing to do seems boring beyond compare). Working at home together, though, has revealed some shortcomings in our lifestyle. We’d be enjoying ourselves more if we had an office - or two - like we did for the first half of our marriage. It would be so helpful to have our own washer and dryer again. We miss having two bathrooms. We’d also really love to have at least one more closet. Each of these desirements adds another notch to the expense of our “dream house” and takes away another notch of our current daily satisfaction. It’s better, so much better, to find ways to be content where we are. Better, cheaper, and easier. Yet there’s that itch to be scratched. If we’re going to continue living and working here, do we really have to do it in a tiny apartment where we carry our laundry up and down three floors every week? Do we really have to sit twelve feet apart while we take calls, with nowhere to go to isolate each other from our background noise? We accepted long ago that we are both ambitious, restless people who aren’t all that good at sitting around and adjusting to the status quo. Might as well acknowledge that we’re ready to un-downsize and give each other another door to shut, a little more privacy. If our future is going to include both of us working from home, then that’s the new baseline. The question is, if we are to buy a house of our own here, a dream house, how are we going to do it? Another question would be, how would you do it where you live? What are all the different ways that you could make that happen?  I love knives, so it made sense to me that a knife would be the symbol of becoming completely debt-free. Not sure if anyone else in the world has ever done this, so I am sharing my idea of the debt knife.

An inkling of the idea of the debt knife probably came from something I read years ago. It was the foreword to a cookbook written by two friends who signed a three-book deal. They did really well off their first book. In the second book, they mentioned that they used some of their money to buy a set of really high-end kitchen knives. ?? I thought. I started my adult life with a bunch of hand-me-downs from various family members and whatever my roommates brought in. I had pots with missing handles, wobbly dull knives, mismatched plates, cracked cutting boards, and melted Tupperware. Nobody was going to offer me a publishing deal on a cookbook because my cooking was terrible. If I wanted to make a recipe and I didn’t have all the ingredients, I would just... skip them. It wasn’t until I’d been married a few years before I discovered that my measuring spoons were inaccurate as well. That explained a lot. It hadn’t really occurred to me, when I read this cookbook by the successful cooking friends, that one would... upgrade one’s gear. Was that... allowed?? Could one simply go out and... buy brand-new stuff? When we got married, my husband’s uncle bought us a really, really excellent soup pot. I love that thing. We have cooked, oh, I’m sure hundreds of gallons of soup in that pot. I think warm thoughts toward that uncle all the time. A close family friend got us a set of salad tongs and likewise, we think about her and her terrific cooking every time we use them. On the other hand, I didn’t think good thoughts about anyone the last time I used our cheap plastic pancake flipper and part of it crumbled off into the pan. Eww. It’s my considered opinion that splurging on small items of daily use is better than other extravagances. For instance, if I buy a very fancy bar of soap, it might cost triple what I’d pay for regular supermarket bar soap, but it’s still under $10 and it will last for months. I’ll enjoy it more than I would an expensive pair of shoes that I would only wear to special occasions - that would then make my feet bleed anyway. This is part of how I’ve gradually developed an appreciation for well-made kitchen gear. This is also part of how I arrived at my debt knife as a symbol of financial freedom. This is how you can tell what a nice knife it is. It came in its own special box and it has a sheath. That’s not how you can tell. You can tell what a nice knife it is because when I showed it to my husband he went “OoooOOOOooo.” Then he wanted to hold it and angle it back and forth. Damascus steel! Lolololol men crack me up, all you have to say is “Damascus steel” or “carbon fiber” and you have their full attention. Try it sometime. What we had been using for the entirety of our marriage were a couple of IKEA knives that I think cost $7 apiece. They were adequate, except that after some time the handles started to dissolve and ooze black goo. Something happened to them after they got cooking oil on them enough times. You’d make dinner and then your hands would turn black. Gross and very annoying. We kept using them, though, because nothing is easier than getting used to small miseries when you’re busy. I though about it and I thought, if I buy one very nice santoku knife, that is all we’ll need. We can chop vegetables with it, then wash it and dry it and put it in its special sheath and put it right back in the drawer. Indeed, that’s exactly what happened. We both like knives and this knife has its own gravitas. The first thing I cut up with the debt knife was... (what would you cut if you had one...?) ...a bunch of kale. I liked the idea of chopping up something that symbolically is flat and rectangular and green, like dollars. I also liked the idea of associating it with a healthy habit like cooking at home. Another thing I like is exploring holiday traditions. For many years now, I’ve been making Hoppin’ John on New Year’s Day. I can’t argue against its claims to bring good luck and financial fortune, because we have gradually done better with money every year since I started making it. Also, at this point I’ve gotten my recipe down to the point of perfection, and sometimes we eat it just because it’s so good with cornbread. Money used to be a painful topic that made me cry. It was like that for many years. In fact, when I met my husband, I was still at the point when I would make a payment on my student loan and the balance would actually be higher because the interest was front-loaded. Many a bitter tear over that. I was so poor I slept on an air mattress that I kept having to patch because I’d wake up on the floor. I haven’t forgotten. Becoming debt-free was a victory that took many years of focus and hard work. It’s something worth celebrating. When you’re still in the trenches, it can feel like it will never happen. It’s so easy to slip into a sense of futility. Don’t give up! Every time I use my debt knife, I think, I did it. I made it through. I will never be in debt again. Every time I use my debt knife, I think, others can do this too. I believe it. Cut yourself free and imagine what symbol you will choose to represent your freedom. |

AuthorI've been working with chronic disorganization, squalor, and hoarding for over 20 years. I'm also a marathon runner who was diagnosed with fibromyalgia and thyroid disease 17 years ago. Archives

January 2022

Categories

All

|

RSS Feed

RSS Feed